Amazon (AMZN) is on track to potentially join the elite $4 trillion market capitalization club, driven by accelerating growth in its cloud computing division, Amazon Web Services (AWS), and increasing profitability in its e-commerce operations. AWS is experiencing a significant AI-driven boost, while strategic improvements in logistics and robotics are enhancing the e-commerce segment’s bottom line. Analysts project a strong earnings growth for Amazon, making a $4 trillion valuation a realistic near-term goal.

The elite club of companies valued at $1 trillion or more is expanding, with Nvidia, Alphabet, and Apple already commanding astronomical figures. While Microsoft briefly joined this exclusive $4 trillion tier late last year, its stock has seen a significant downturn. However, a new contender is emerging: Amazon (AMZN). With its market capitalization at $2.9 trillion as of Wednesday, May 13, Amazon is poised to potentially join the $4 trillion club, offering investors an anticipated 38% return.

Accelerating Growth at Amazon Web Services (AWS)

Amazon Web Services (AWS), the world's leading cloud computing platform, is experiencing a significant surge in revenue growth, largely propelled by the artificial intelligence (AI) revolution. AWS provides a vast array of services essential for businesses in the digital age, from data storage and web hosting to sophisticated software development and data analytics. Its growing importance as a hub for AI software development is directly fueling its impressive revenue acceleration.

AI presents a multi-faceted opportunity for AWS. Firstly, businesses require substantial computing power to deploy AI software, which AWS delivers through its global network of data centers. While AWS utilizes advanced chips from third-party suppliers like Nvidia, it also develops its own proprietary hardware. The company's latest Trainium2 chip offers a 30% price-performance improvement over competitors, with the upcoming Trainium3 promising an additional 40% enhancement. Notably, Amazon has secured $225 billion in revenue commitments from customers eager to rent these custom AI chips, marking it as one of the company's most successful product platforms to date.

Furthermore, AWS Bedrock provides businesses with access to cutting-edge, ready-made foundation models from AI pioneers such as OpenAI and Meta Platforms, streamlining AI software development projects. By the end of Q1 2026 (ending March 31), Bedrock had amassed over 125,000 customers, with spending increasing by an astonishing 170% from the previous quarter. Overall, AWS reported $37.5 billion in revenue for Q1, a 28% year-over-year increase – its third consecutive quarter of accelerated growth, underscoring its strong AI momentum.

The future looks even brighter for AWS, as the platform ended Q1 with an immense $364 billion in pending customer orders for future infrastructure deployment. This figure does not include an additional $100 billion from a recent agreement with AI startup Anthropic.

E-commerce Profitability Surges

While AWS captures much of the spotlight, Amazon's foundational e-commerce business is also demonstrating robust performance. Both its online stores and third-party seller services saw accelerating revenue growth in the first quarter, both sequentially and year-over-year. However, the most striking improvement has been in profitability.

Combined, Amazon's North American and international e-commerce segments generated $9.7 billion in operating income in Q1, marking a significant 47% increase from the prior year. This improvement stems from strategic initiatives like the 2023 split of its American fulfillment network into eight regions, shortening delivery distances and reducing logistics costs, thereby enhancing profit margins. Furthermore, Amazon's ongoing investments in robotics are boosting productivity within its fulfillment centers, providing another significant boost to its bottom line.

Key Data Points

Amazon's Mathematical Pathway to $4 Trillion

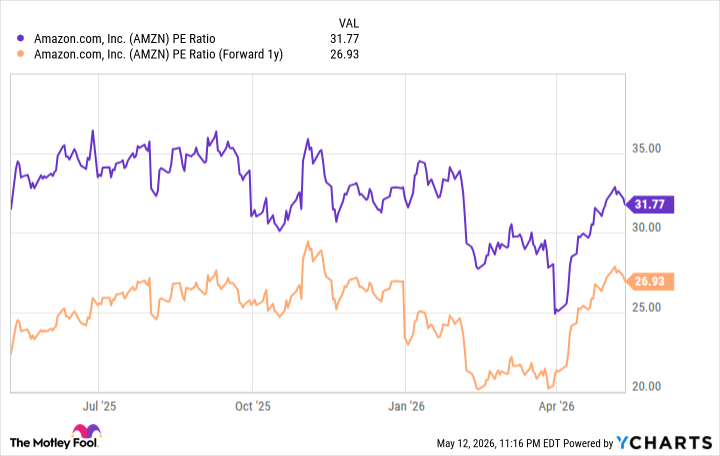

Amazon's stock currently trades at a price-to-earnings (P/E) ratio of 31.7, based on its trailing-12-month earnings of $8.37 per share. This valuation is slightly lower than the Nasdaq-100 index's P/E ratio of 35.6, suggesting potential undervaluation relative to its tech peers. Wall Street analysts project Amazon's earnings to reach $9.87 per share by 2027, placing its forward P/E ratio at 26.9.

For Amazon's stock to reach a $4 trillion market capitalization, it would need to appreciate by approximately 38% from its current valuation. This growth trajectory would see its market cap fall between $3.37 trillion and $3.77 trillion if it were to maintain its current P/E ratio or trade in line with the Nasdaq-100's current P/E, respectively. Given that Amazon's P/E ratio has historically exceeded 35 for extended periods, the higher end of this range appears entirely attainable.

Achieving a $4 trillion valuation would then require only a modest 6% earnings growth in 2028, a target well within reach considering Wall Street's more optimistic projections of earnings growth exceeding twice that rate in both 2026 and 2027. This analysis suggests Amazon has a strong probability of entering the $4 trillion club within the next two and a half years.

: Why Its Current Valuation Might Be Too Risky for Investors")