Meta Platforms (META) is implementing a new strategy to monetize its substantial AI investments, aiming to boost its underperforming stock. The tech giant is rolling out subscription services across its social media platforms and for its AI offerings, seeking to justify billions in capital expenditure.

With its core ad business showing strong growth driven by AI, Meta is now banking on recurring revenue from subscriptions to enhance its valuation and market position.

Meta's AI Monetization Play: Can Subscriptions Revive Underperforming Stock?

Meta Platforms (META) is facing a year-to-date stock performance lag, underperforming the broader market and many of its 'Magnificent 7' peers. While its core advertising business shows strength, driven by AI-powered personalization, the company's massive investments in artificial intelligence are under market scrutiny. Meta is now rolling out a multi-pronged strategy involving new subscription services to monetize its AI efforts and justify its significant capital expenditures.

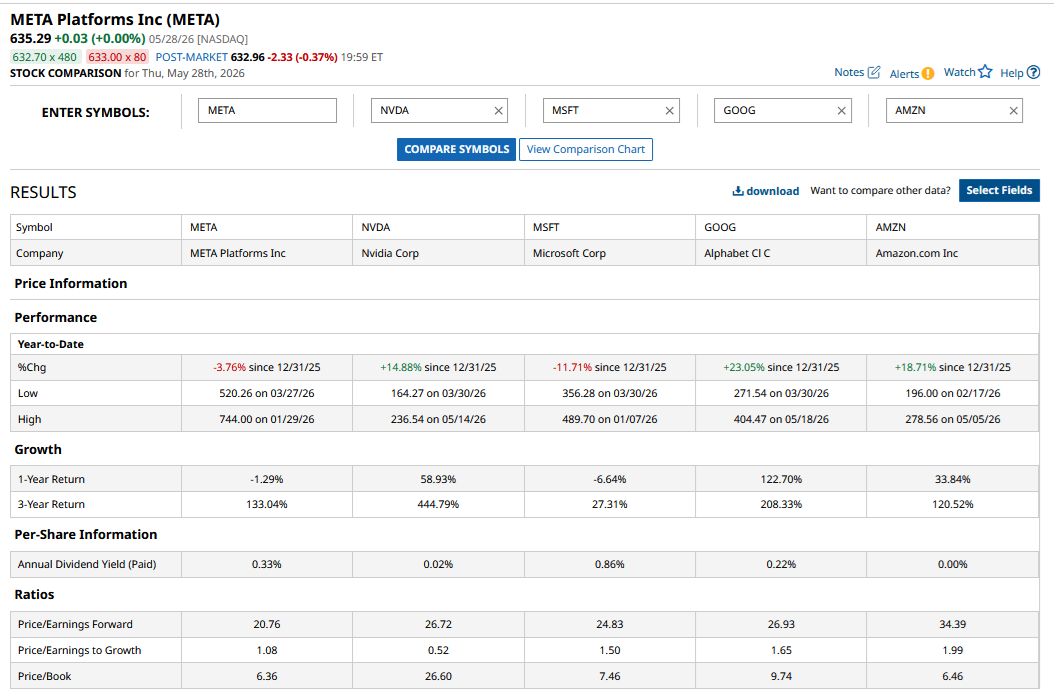

Meta Platforms (META) is currently experiencing a year-to-date stock performance of -4.66%, placing it behind the market's overall gains and trailing most of its 'Magnificent 7' counterparts. Only Microsoft (MSFT) has seen a worse performance among this elite group. This divergence in stock performance is largely attributed to market sentiment regarding each company's artificial intelligence (AI) initiatives. While Alphabet (GOOGL) has impressed with its AI advancements and robust core businesses, Meta's considerable AI investments are being closely watched.

AI's Impact on Meta's Revenue and Capex

Despite stock market concerns, Meta's advertising business has been performing exceptionally well. In the first quarter of 2026, the company reported a 33% year-over-year revenue increase, the highest growth seen since 2021. This surge is significantly fueled by AI-driven personalized advertising. While this growth is impressive, Meta faces a unique challenge compared to cloud-centric hyperscalers like Microsoft and Amazon. Unlike its peers, Meta lacks a substantial in-house cloud operation, making it harder to validate its escalating capital expenditures, which are projected to be between $125 billion and $145 billion. This substantial investment, double that of 2025 at the higher end, is under intense market scrutiny regarding its monetization potential.

Meta's New Subscription Strategies

To address market concerns and generate new revenue streams, Meta is actively pursuing monetization strategies for its AI investments. Beyond existing offerings like Meta Verified and ad-free European subscriptions (launched primarily for regulatory compliance), the company is launching new subscription tiers across its major platforms: Instagram, Facebook, and WhatsApp. These subscriptions will offer enhanced features such as profile customization and super reactions, priced at $3.99/month for Instagram and Facebook, and $2.99/month for WhatsApp.

Furthermore, Meta is introducing two specific AI-focused subscriptions: Meta One Plus at $7.99/month and Meta One Premium at $19.99/month. These initiatives are crucial for recouping the billions invested annually in AI model development and justifying the company's significant capital expenditure. While Meta's current subscription revenue is minimal, comprising less than 2% of Q1 revenue within its 'Other' segment, the expansion of these services represents a strategic pivot towards recurring revenue.

Outlook for Meta's Subscription Success

The success of Meta's subscription strategy hinges on its ability to offer compelling value to its vast user base of over 3.5 billion daily active users. While initial adoption may be slow, the company has the potential to enhance subscriber-only features and gradually limit certain functionalities for non-paying users, incentivizing upgrades. The AI-specific subscriptions align with the industry trend of charging for premium AI capabilities. Long-term, these recurring revenues are expected to be a significant growth driver and a key factor in supporting Meta's valuation.

Investment Perspective on META Stock

Meta Platforms is currently trading at a forward price-to-earnings (P/E) multiple of 20.7x, the lowest among its 'Magnificent 7' peers. This attractive valuation, coupled with analyst expectations of a nearly 19% EPS increase in 2026, suggests potential upside. Despite current earnings being impacted by Reality Labs losses, the company's optimistic outlook for 2026 operating income and the strategic introduction of subscription services strengthen the bullish case for Meta stock.

: Why Its Current Valuation Might Be Too Risky for Investors")