/https://media.cnbc.com/dims/origin/108343257/Spider-Man-Brand-New-Day.jpg "Spider-Man Smashes Box Office Records with ‘Brand New Day’ Preview Haul")

Amazon is poised to join an elite group of $4 trillion companies, currently occupied by Nvidia, Alphabet, and Apple. Driven by the accelerating growth of its cloud computing arm, AWS, fueled by artificial intelligence, and the increasing profitability of its dominant e-commerce platform, Amazon presents a compelling investment case. With a current market capitalization of $2.9 trillion, the company could see a significant return as it charts a path to this unprecedented valuation.

Only a select few companies inhabit the ultra-exclusive $4 trillion market capitalization club in the U.S., with Nvidia, Alphabet, and Apple currently holding the prestigious titles. While Microsoft enjoyed a brief tenure last year, its stock has since seen a notable decline. However, a formidable contender is emerging with a clear path to join this elite group: Amazon (AMZN).

As of the market close on Wednesday, May 13, Amazon commanded a market capitalization of $2.9 trillion. This implies a potential 38% return for investors should the company successfully cross the $4 trillion threshold, driven by the remarkable performance of its core businesses.

Image source: The Motley Fool.

Accelerating Momentum at Amazon Web Services

Amazon Web Services (AWS) reigns as the world's leading cloud computing platform, offering a vast array of services vital for businesses navigating the digital era. From fundamental data storage to advanced software development, AWS is now a primary destination for enterprises developing and deploying AI software, a factor significantly fueling its revenue growth acceleration.

AI presents a multi-faceted opportunity for AWS. First, businesses require immense computing power to run AI applications, which AWS provides through its global network of data centers. While relying on advanced chips from partners like Nvidia, Amazon has also innovated with its own silicon. Its latest Trainium2 chip boasts 30% better price performance than rivals, with the forthcoming Trainium3 promising an additional 40% improvement. Amazon has already secured a staggering $225 billion in revenue commitments from customers eager to leverage Trainium chips, establishing it as one of the company's most successful product launches.

Further enhancing its AI offering is AWS Bedrock, a platform where businesses can access cutting-edge foundation models from top developers such as OpenAI and Meta Platforms, accelerating their AI development projects. By the end of the first quarter of 2026 (March 31), Bedrock served over 125,000 customers, who increased their spending by an astounding 170% from the previous quarter.

Overall, AWS reported $37.5 billion in revenue for the first quarter, marking a 28% increase year over year. This growth rate has accelerated for the third consecutive quarter, underscoring the platform's robust AI-driven momentum.

Even more rapid expansion appears to be on the horizon for AWS, which concluded the first quarter with an astounding $364 billion in customer orders awaiting the deployment of additional data center infrastructure. This figure doesn't even account for an extra $100 billion stemming from a recent partnership between AWS and AI start-up Anthropic.

E-commerce Becomes a Significant Profit Driver

While AWS garners much-deserved attention, Amazon's foundational e-commerce business is experiencing a quiet resurgence. Its online stores and third-party seller services particularly shone in the first quarter, both exhibiting accelerating revenue growth on a sequential and year-over-year basis. However, the true highlight was the impressive surge in profitability.

The combined North American and international e-commerce segments generated $9.7 billion in operating income during the quarter, a remarkable 47% increase from the prior-year period. This significant boost is largely attributed to strategic operational improvements. In 2023, Amazon decentralized its American fulfillment network into eight distinct regions, dramatically shortening delivery distances and consequently reducing logistics costs, which has directly enhanced the company's profit margins. Furthermore, substantial investments in robotics are bolstering productivity across its fulfillment centers, creating another powerful tailwind for the bottom line.

Amazon's Clear Financial Trajectory to the $4 Trillion Club

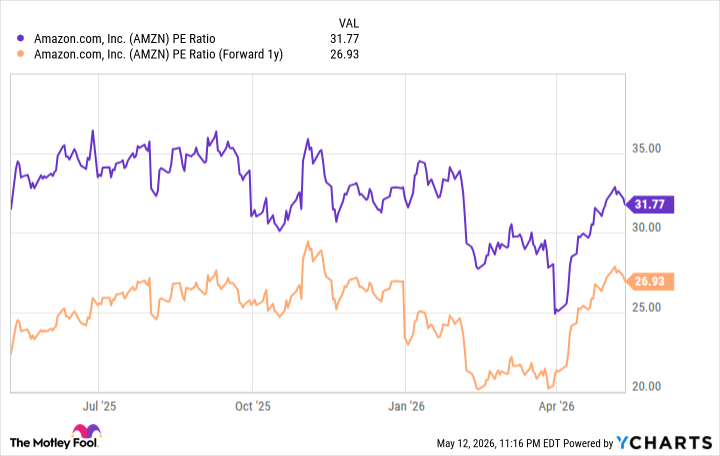

Based on Amazon's trailing-12-month earnings of $8.37 per share, its stock currently trades at a price-to-earnings (P/E) ratio of 31.7. This valuation positions it more affordably than the Nasdaq-100 index, which trades at a P/E ratio of 35.6, suggesting Amazon may be undervalued compared to its big-tech counterparts.

Looking ahead, Wall Street analysts project Amazon's earnings to climb to $9.87 per share by 2027 (according to Yahoo! Finance), which would place its stock at a forward P/E ratio of 26.9.

Data by YCharts.

To maintain its current P/E ratio of 31.7, Amazon's stock would need to climb by 18% before the end of next year. To align with the Nasdaq-100's current P/E, it would require a 32% increase. These scenarios would place its market capitalization between $3.37 trillion and $3.77 trillion. Considering Amazon's P/E ratio often exceeded 35 for a significant part of the past two years, the higher end of this projected range is entirely plausible.

If the company reaches this point, it would only need an additional 6% in earnings growth in 2028 to justify a $4 trillion valuation – a relatively modest target, especially when juxtaposed with Wall Street's predictions of more than double that growth rate for both 2026 and 2027. This strong financial trajectory suggests that Amazon has an excellent chance of joining the exclusive $4 trillion club within the next two-and-a-half years.

: Why Its Current Valuation Might Be Too Risky for Investors")